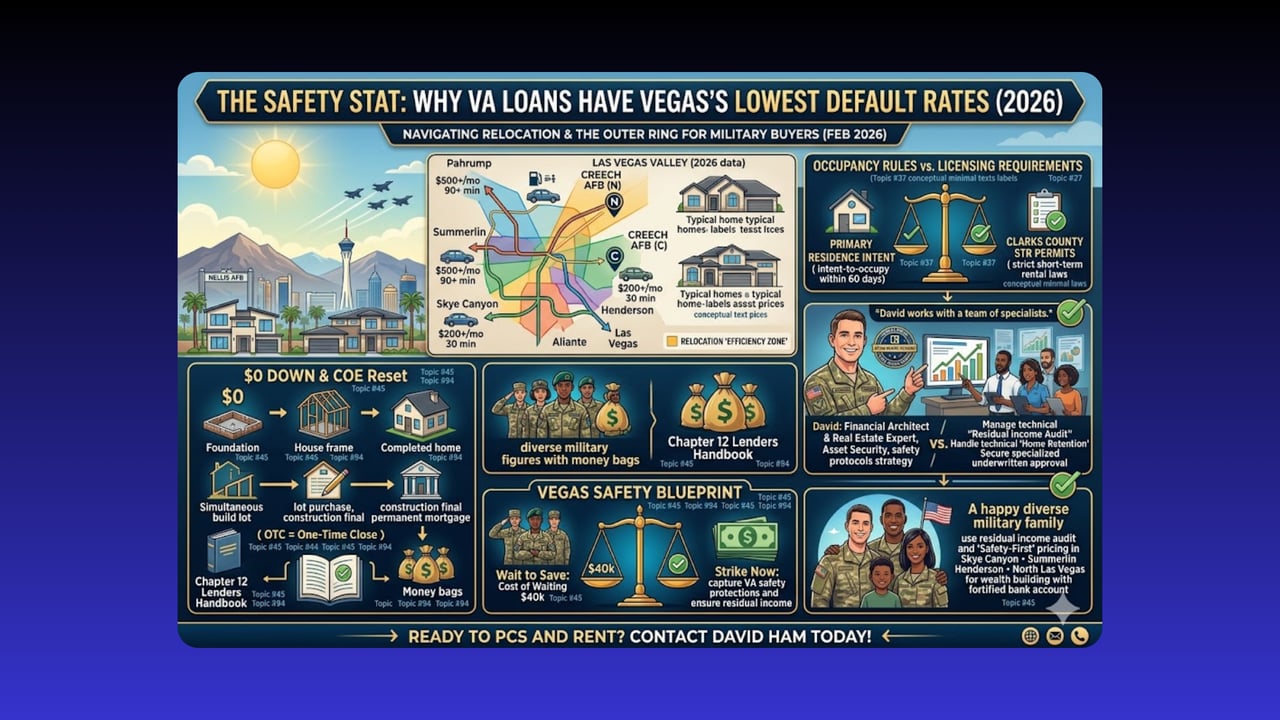

The Safety Stat: Why VA Loans Have Vegas’s Lowest Default Rates

It often sounds too good to be true: $0 down, flexible credit standards, and no monthly PMI—yet VA loans consistently maintain the lowest foreclosure and default rates of any mortgage product in the country. In March 2026, VA loans continue to significantly outperform conventional loans in the Las Vegas valley. This isn't by accident; it’s because the VA program is built with a "Safety-First" architecture that protects the Veteran’s home as much as it protects the lender’s investment.

I am David Ham. Alongside my dedicated team of specialists, we act as your "Financial Architects," utilizing these safety protocols to ensure your 2026 home purchase is built on a foundation of permanent stability.

Key Takeaways for the 2026 Safety Advantage

-

The Residual Income Power (Topic #45): Unlike conventional loans that only look at your debt-to-income (DTI) ratio, the VA is the only 2026 product that enforces a Residual Income Test. This ensures that after your mortgage, taxes, and debts are paid, you still have a specific "cushion" of cash for gas, groceries, and family life. In 2026, the requirement for a family of four in the West is $1,117, providing a built-in safety net against inflation.

-

Strict "Anti-Toxic" Protections: VA loans are intentionally simple. Under 2026 guidelines, they are prohibited from containing "toxic" features like balloon payments, prepayment penalties, or adjustable rates that could trap a homeowner in a rising-rate environment. You get a stable, fixed-rate product that you can rely on for the life of the loan.

-

Aggressive Home Retention (Topic #94): If you face a legitimate 2026 hardship, you aren't alone. The VA Home Loan Program Reform Act of 2025 solidified the VA's Home Retention team as the most aggressive in the business. They provide "Partial Claim" options and mediation that conventional lenders simply do not offer, with the goal of keeping you in your home at all costs.

-

The Veteran Discipline Factor: Statistically, the same mission-first mindset and financial discipline that served you in uniform translate directly to homeownership. Lenders in 2026 recognize that Veterans are statistically superior borrowers, which is why they often offer lower interest rates for VA products than for conventional ones.

The 2026 "Safety Savings" Reality

In the current Las Vegas market, lenders "price for risk." Because VA loans are backed by the federal government and protected by residual income standards, they are considered the lowest-risk assets in a lender's portfolio. We leverage these "Safety Stats" to negotiate the lowest 2026 interest rates and most favorable terms for our clients, turning the program’s safety into your financial gain.

Your Financial Architect & Real Estate Team

I am your Financial Strategy and Real Estate Expert. While my trusted team of specialists handles the technical "Residual Income Audit" and manages the lender-side "Safety-First" pricing models, I focus on your "Asset Security."

We don't just "get you approved"; we ensure you are approved for a payment that allows your family to thrive in Skye Canyon, Summerlin, or Aliante. I’ll show you how the 2026 safety protocols protect your equity during market shifts, ensuring your home remains a source of wealth, not a source of stress. We build your 2026 mortgage with the same precision you’d expect from a mission plan.

Ready to Build a Secure 2026 Future?

Don't settle for a "standard" mortgage when you’ve earned the safest one on the market. Let’s architect your 2026 plan today. Contact David Ham, your Active military, veteran and VA real estate expert today, and my team and I will provide our exclusive "2026 Las Vegas Financial Stability Report" to get you started!